How to Audit a Commercial Real Estate Underwriting Model.

The eight checks we run when we rebuild a sponsor's underwriting model in a second engine, and the specific error that each one is built to catch first.

Most bad deals are not bad ideas. They are good ideas wearing a model that flattered them. The rent roll double counted a suite. The waterfall allocated every dollar and still cleared the promote. The refinance assumed today's rate three years out. None of it was fraud. It was arithmetic nobody recalculated in a second engine.

Auditing a model is not glamorous and it is not optional. Here is the discipline we use when we rebuild a client model beside their own and reconcile every number to the source once.

1. Rebuild the revenue from the rent roll, do not trust the summary

Start at the rent roll, not the pro forma. Sum the square footage yourself and tie it to the offering memorandum. Sum the in-place rent and divide by the square footage to get an implied rent per square foot, then sanity check it against the market. The most common error in the business is a suite counted twice or a vacant unit carried at market rent with no downtime. If the going-in yield looks 30 to 40 basis points too good, this is usually why.

The scale of the error is easy to underestimate. Take a 100,000 square foot building at 18 dollars a foot. One 4,000 square foot suite counted twice adds 72,000 dollars of phantom revenue, and at a 6.5 percent cap rate that is about 1.1 million dollars of value that does not exist. Nobody catches it by staring at the summary tab because the summary tab is where the error lives. You catch it by re-adding the rent roll yourself. While you are there, check the lease expiration schedule against the hold period. A model that shows no rollover downtime during years when a third of the rent roll expires is not conservative, it is unfinished.

2. Trace every operating expense to a source

Expenses are where optimism hides. Reconcile each line to the trailing twelve months, not to a ratio. Watch for taxes underwritten at the current assessment rather than the reassessment a sale will trigger, management fees quoted below market, and a repairs line that assumes the building will behave better under new ownership than it did under old. A clean model states its expense assumptions plainly and survives a reader asking "says who."

Taxes deserve their own sentence because they are the largest single line on most operating statements and the one a sale changes mechanically. In many jurisdictions the assessor marks the property to something near the sale price, so underwriting the seller's tax bill on a building trading well above its assessment builds a six figure hole into year one. The fix is not a guess. Pull the jurisdiction's reassessment practice and the millage, compute the post-sale bill and put the working in the model where a reader can check it.

3. Recompute the NOI bridge, line by line

Net operating income is the number everything else rides on, so recompute it independently. Gross potential rent, less vacancy and credit loss, plus other income, less operating expenses. Do it in a fresh cell block, not by trusting the model's own total. A single mislinked cell here moves the valuation by hundreds of thousands of dollars. A 25,000 dollar error in NOI at a 6.5 percent cap rate is roughly 385,000 dollars of price, which is why the bridge gets rebuilt rather than reviewed. If your recomputed NOI and the model's NOI differ by even a dollar, stop and find out why before touching anything downstream. Small unexplained differences are how large hidden ones announce themselves.

4. Size the debt to all three constraints

Lenders quote loan to value, debt service coverage and debt yield, and your proceeds are set by whichever binds. Run all three. If the model sizes to LTV and assumes that controls, stress the interest rate 75 basis points and watch coverage take over. Proceeds are a rate bet whether the model admits it or not. A model that sizes to only one constraint is not finished.

Worked example, assumptions stated: 950,000 dollars of NOI, a 1.25x coverage requirement and a 30 year amortization. At 6.5 percent the loan constant is about 7.6 percent and coverage supports roughly a 10.0 million dollar loan. Move the rate to 7.25 percent and the constant rises to about 8.2 percent, which cuts the supportable loan to roughly 9.3 million. That is a 7 percent haircut to proceeds from a rate move well inside a normal quarter, and every dollar of it comes out of the equity check or the deal dies. If the model cannot show you that sensitivity on one screen, it is hiding the deal's real risk.

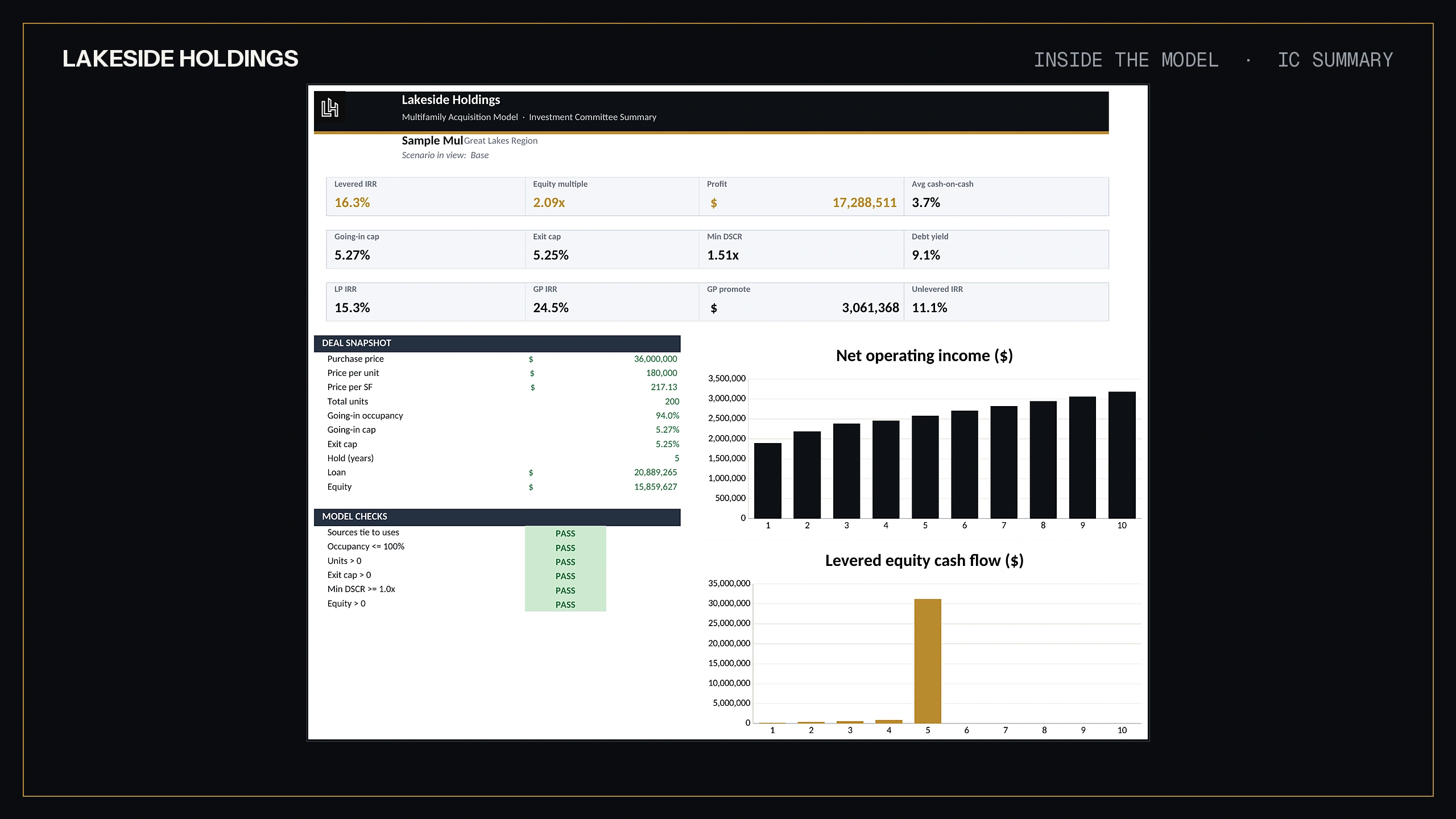

Exhibit · The committee summary, every output the eight checks have to survive · Multifamily Acquisition Model

5. Check the amortization actually amortizes

Pull the loan balance at the end of the hold and confirm it matches an independent amortization schedule. Interest-only periods, mis-entered terms and a constant that does not match the rate all show up here. On a refinance deal, confirm the model is not quietly assuming the acquisition rate at a future refinance.

6. Stress the exit cap, because it does most of the work

In a five year hold the exit cap is quietly responsible for most of the outcome. Buy at a 6.0 cap on a million of NOI, grow it three percent a year, and selling at a 7.0 exit can leave the building worth less than you paid even though income rose. Never accept an exit tighter than entry without a reason you would say out loud to an investor, and always price the deal at entry plus 50 and plus 100 basis points. If the basis does not survive both, the deal is a bet on cap rate compression, not on operations.

7. Prove the waterfall allocates exactly 100 percent

Sum every distribution tier and confirm the cash out equals the cash available, no more and no less. Confirm the preferred return compounds the way the agreement says, that the promote hurdles are in the right order, and that the sponsor catch-up does not begin before the limited partner is made whole. A waterfall that clears the promote while over-allocating cash is the single most expensive spreadsheet error in private real estate.

Two details deserve extra suspicion. First, compounding basis: an 8 percent preferred return compounded annually and one accrued simple diverge more every year the deal runs long, and the operating agreement picked one. Second, hurdle measurement: an IRR hurdle and an equity multiple hurdle can disagree about whether the promote has been earned, especially after a refinance returns capital early. The model must implement the document, not a generic template's memory of one. Read the distribution section of the agreement with the model open and tie every tier to a clause.

8. Run the model hostile inputs and see if it breaks

A good model fails loudly, not silently. Enter a vacancy of zero, then of fifty percent. Enter a negative rent. Enter an exit cap of two percent. A disciplined model flags the nonsense or holds its logic. A fragile one returns a confident wrong number, which is exactly what it will do at one in the morning when an analyst fat-fingers a cell.

The practical version of this check is a row of audit flags that live in the model permanently: sources equal uses, the loan balance ties to the schedule, the waterfall allocates 100.0 percent, square footage ties to the rent roll, every distribution is non-negative. Green when true, loud when not. Models we release are verified against an independent replica before release, and the audit rows exist so the model keeps re-verifying itself every time someone changes an input after we let go of it.

The principle underneath all eight

Audit the model in a second engine, reconcile every number that reaches an investor to its source once and make the model fail loudly. That is the whole discipline. It is boring, and it is the difference between a disciplined deal and a quiet disaster.

Notice what is not on the list: opinions about the market. An audit is not a debate about whether rents grow at two percent or three. It is a verification that the model does what its own assumptions say it does, that every input has a source and that the arithmetic between input and conclusion is intact. Keep the two arguments separate. A deal team can disagree about the future and still agree the model is telling the truth about the present.

We use an essential cookie to remember your preferences and privacy-first analytics that collect no personal data. By continuing you accept our Cookies Policy.We use one essential cookie and privacy-first analytics. Read the Cookies Policy.