How to size a construction loan before the term sheet does it for you.

A construction loan is sized three times: by your model, by the lender's screen and by reality during the draw. How to make all three agree first.

A construction loan is sized three times. Once by your model, once by the lender's screen and once by reality during the draw period. The goal of underwriting is to make all three agree before you sign anything.

The one constraint that matters at close

Construction lenders quote leverage as loan to cost. The trap is the denominator: total project cost includes the financed origination fee and the capitalized interest reserve, and both of those depend on the loan amount you are trying to solve for. Sponsors who bolt this onto an acquisition model end up with a circular reference and an iterative solver that breaks the first time someone changes a date.

There is a closed-form answer. Write total cost as hard and soft costs plus the fee and reserve expressed as fractions of the commitment, then solve for the commitment directly. One algebra step kills the circularity forever, which is exactly how our Construction Loan Module sizes to LTC with no iteration and no fragile solver settings.

The reserve is a forecast, not a plug

Capitalized interest is where construction models flatter deals. Interest accrues monthly on the outstanding balance, and the balance follows your draw curve. Draw hard costs on an S curve, which is how real projects spend, and the balance stays low early, which means a smaller reserve than a straight-line guess would suggest. Draw straight-line in the model while the project actually spends on an S curve and your reserve is oversized, your equity requirement overstated and your returns understated. Reverse the mistake and you run out of reserve in month fourteen, which is a phone call nobody enjoys.

The discipline: model the draw schedule at the line-item level, accrue interest monthly on the actual projected balance and then test the reserve against that accrual. If the reserve fails the test, the model should say so in red before the lender says so in a default notice.

Equity first, always

Institutional construction debt funds after equity is fully spent. Your model must burn equity to zero before the first dollar of debt draws, because that is how the loan agreement will read. This ordering changes the interest math, the peak balance and the true cost of the project. A model that draws debt and equity pro rata from day one is wrong in the lender's favor early and wrong in yours late.

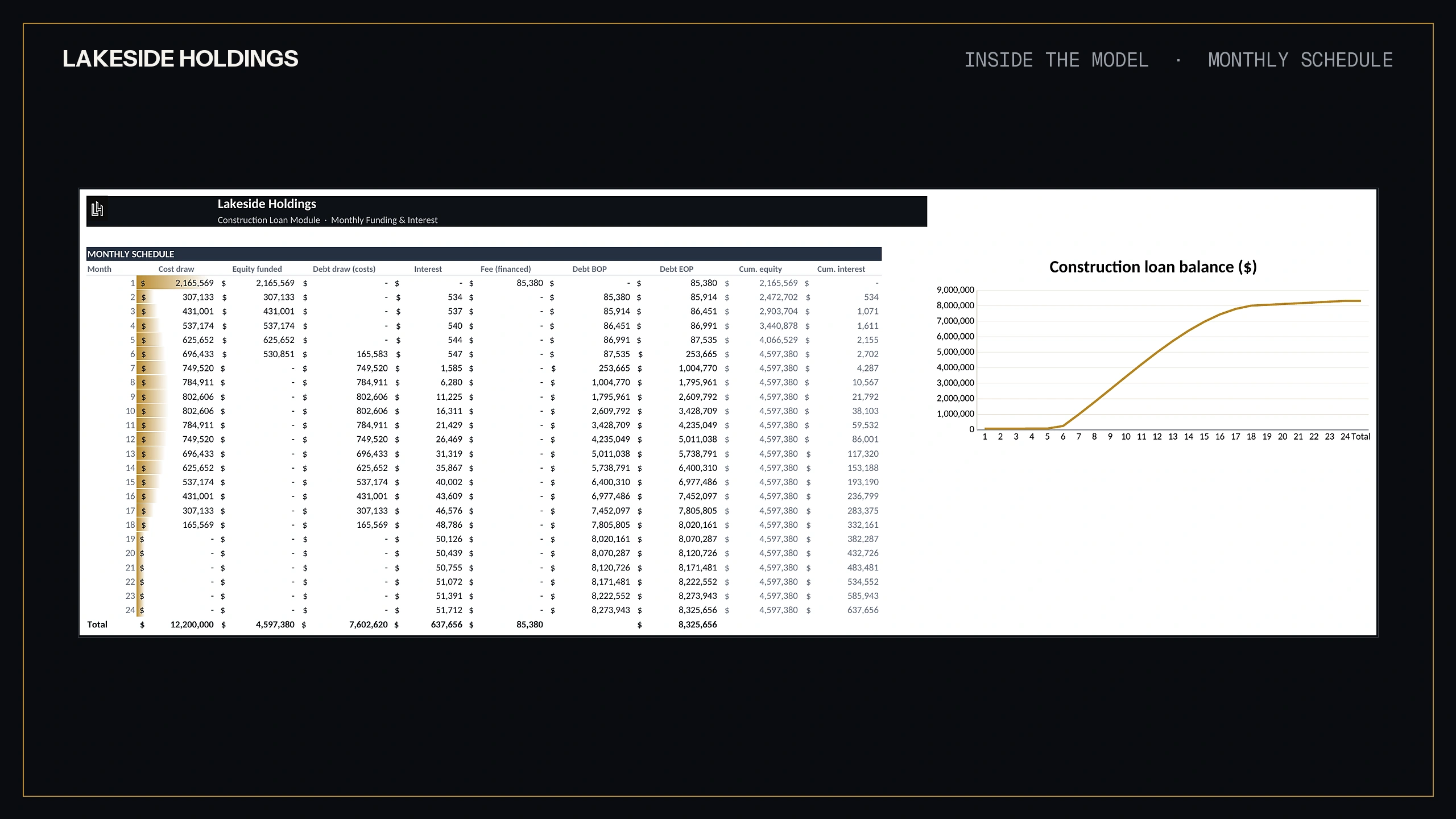

Exhibit · Monthly funding, equity first, with the interest reserve accruing in the open · Construction Loan Module

The worked sequence

State the budget: land, hard costs, soft costs, each with its own timing. Pick the curve per line: S curve for hard costs, straight-line for most soft costs, upfront for land and fees. Size the commitment closed-form to your LTC on total cost including the financed fee. Fund equity first, then debt. Accrue interest monthly on the balance. Capitalize it against the reserve and test the reserve every month. Read the outputs that matter: peak balance, total interest, actual LTC at completion and the sources and uses tie-out, which must balance to the dollar.

If the tie-out is off by even one dollar, something upstream is broken and every downstream number is decoration. Our module carries the tie-out as a permanent check row, PASS or CHECK, because a model that cannot prove its own arithmetic should not be trusted with yours.

What the lender will do to your number

Whatever you size, the lender will stress it: higher rate on the accrual, slower absorption, a contingency draw you did not plan. Run the same stresses first. If a 75 basis point rate stress blows through your reserve, resize the reserve now, when it costs a formula change, not in month sixteen when it costs a capital call.

The model decides the deal. The Construction Loan Module and the Construction Draw Schedule are built for exactly this workflow and they are in the library.

For informational and educational purposes only. Not investment, legal or tax advice.

Put it to work

The models behind these essays are in the library.

We use an essential cookie to remember your preferences and privacy-first analytics that collect no personal data. By continuing you accept our Cookies Policy.We use one essential cookie and privacy-first analytics. Read the Cookies Policy.