Insights · Underwriting · July 2026 · 6 min

The Exit Cap Does Most of the Work in Your IRR.

The assumption doing the most work in your model is usually the one with the least underneath it. What the exit cap is really worth, priced in dollars.

The assumption doing the most work in your model is usually the one with the least underneath it. What the exit cap is really worth, priced in dollars.

Ask a deal team to defend their rent growth assumption and you will get a market study. Ask them to defend their expense ratio and you will get a T-12. Ask them to defend the exit cap rate and, more often than anyone admits, you will get a shrug and the phrase "we held it flat." The assumption doing the most work in the model is the one with the least underneath it.

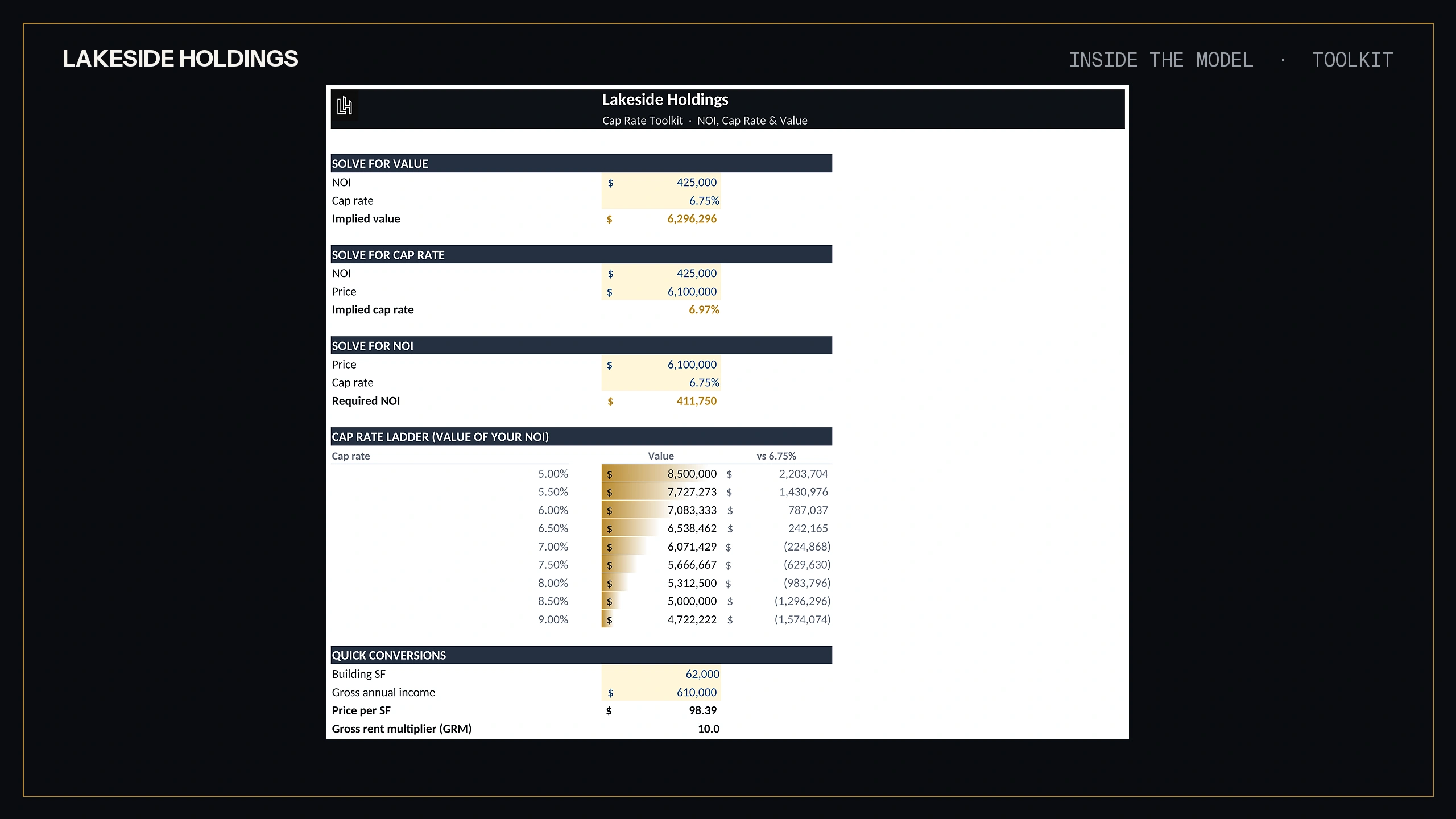

Here is the uncomfortable arithmetic. In a five year hold, the sale typically returns the large majority of the cash the deal ever produces. The sale price is NOI divided by the exit cap. So one number, chosen years before the market it describes exists, sits under most of your IRR. It deserves more than a shrug.

Assumptions stated plainly: buy a property at a 6.0 percent cap on 1,000,000 dollars of in-place NOI, so a 16.67 million purchase. Grow NOI 3 percent a year for five years, which is honest work, to about 1.16 million.

Sell at the same 6.0 cap and the building fetches about 19.3 million. Call it 2.7 million of appreciation earned by operations.

Now sell at a 7.0 cap instead. The same 1.16 million of NOI prices at about 16.6 million. That is roughly 100 basis points of cap expansion, and it just consumed five years of three percent NOI growth and handed back slightly less than the purchase price. Every dollar of operational improvement, real work, real capital, real risk, was erased by one input moving one point. Leverage makes the equity math uglier still, since the debt does not shrink because the exit widened.

Run it the other direction and the flattery is just as strong. Exit at 5.5 and the model prints a 21 million sale and a beautiful IRR, built not on the deal but on the assumption that buyers three years from now will pay more per dollar of income than you did. That is not underwriting. That is a position in future interest rates wearing an operations costume.

The exit cap is a forecast of what a future buyer will pay per dollar of your future income. It compresses everything you cannot know, rates, capital flows, the asset's age, the market's mood, into one divisor. Which is why the discipline around it matters more than the point estimate. You will not guess it correctly. The goal is to make sure the deal does not require you to.

Three rules give the number the respect it deserves.

First, never underwrite an exit tighter than entry without a reason you would say out loud to an investor. There are legitimate ones: a lease-up completed, a property repositioned into a different buyer pool, submarket infrastructure that is funded and under construction rather than rumored. "The market should recover by then" is not on the list. If the reason embarrasses you in a sentence, it does not belong in a cell.

Second, age the asset. A common convention adds around 5 to 10 basis points to the exit cap per year of hold, reflecting that you are selling an older building into a market that will compare it against newer stock. Treat the convention as a floor for your thinking, not a substitute for it. A 1980s asset with original systems widens faster than a 2020 build.

Third, price the deal at entry plus 50 and plus 100 basis points, every time, on one screen. Not as a downside case buried in a scenario tab nobody opens. As a standing exhibit next to the base case. If the basis survives entry plus 100, the deal is resilient to the thing you cannot control. If it only works at exit flat or tighter, you are not buying a building, you are buying a cap rate forecast, and you should size your conviction accordingly.

When we audit a model, the exit cap section is where optimism goes to dress up. The patterns repeat. A sensitivity table that stresses rent growth and vacancy in fine grain but holds the exit cap fixed, which stresses the small levers and parks the large one. An exit cap keyed to "entry minus 25" so improving the purchase price quietly improves the exit. Terminal value computed on year five NOI instead of the forward year a buyer would actually price, which borrows a year of growth the seller does not own. And the quiet one: refinance proceeds in year three computed at today's rate, which is the same bet as a tight exit cap wearing a different hat.

None of these are fraud. They are defaults nobody challenged. But a model that will not show you entry plus 100 on the same screen as the base case is hiding the deal's real risk, and it is usually hiding it from the sponsor first. The fix is structural, not moral: build the model so the stress is always visible and the flattery has nowhere to sit. That is how the models in our library are built, and it is one of the checks in our model audit when the file is somebody else's.

Before the next committee meeting, try this. State the exit assumption as a sentence about a human being: "A buyer in 2031 will pay us more per dollar of income for this 45 year old building than we paid in 2026." If the sentence sounds reasonable, defend it with evidence. If it sounds like a hope, reprice the deal at entry plus 50 and plus 100 and see whether you still want it. The Underwriting Memo walks through this discipline in full, and the free screener will show you in five minutes which side of the line a deal sits on.

Cap rate compression is a gift when it arrives. It is a business plan only by accident. Underwrite the operations, stress the exit and let the deal prove it does not need the gift.

The model decides the deal.

We use an essential cookie to remember your preferences and privacy-first analytics that collect no personal data. By continuing you accept our Cookies Policy.We use one essential cookie and privacy-first analytics. Read the Cookies Policy.