Insights · Debt · July 2026 · 7 min

Three Constraints Walk Into a Term Sheet.

Every term sheet quotes three constraints. Your proceeds are set by whichever one binds, and you do not know which one binds until you run all three.

Every term sheet quotes three constraints. Your proceeds are set by whichever one binds, and you do not know which one binds until you run all three.

Every term sheet quotes three constraints. Loan to value. Debt service coverage. Debt yield. Sponsors read them as three versions of the same number and anchor on whichever is most familiar, usually LTV, because LTV is the one that sounds like a decision you get to make. It is not. Your proceeds are set by whichever constraint binds, and you do not know which one binds until you run all three. Sponsors who assume LTV controls get retraded by their own leverage assumption, politely, at the worst possible moment in the deal.

The three constraints are not rivals. They are three different creditors' questions wearing one term sheet. LTV asks what the collateral is worth if the lender has to take it back. Coverage asks whether the property's cash flow can carry the payments with room to stumble. Debt yield asks what return the lender earns on its own basis if it owns the building tomorrow, with no help from an appraiser and no opinion about interest rates. Each one caps the loan from a different direction, and the loan you actually get is the smallest of the three answers.

Loan to value is the simple one: a percentage of appraised value. At 65 percent LTV against a 10 million dollar appraisal, the ceiling is 6.5 million. Note what it depends on, an appraisal, which is an opinion about a market, which moves. LTV feels like the sponsor's constraint because it is the one quoted in marketing. It is also the one the lender trusts least, for exactly that reason.

Debt service coverage works backward from cash flow. The lender sets a minimum ratio of net operating income to annual debt service, commonly 1.20 to 1.30 for stabilized assets. Divide NOI by the required ratio and you get the maximum payment the property is allowed to carry. Divide that payment by the mortgage constant, the annual debt service per dollar of loan at the quoted rate and amortization, and you get the maximum loan. Two things move this number: the property's NOI and the interest rate. Only one of them is yours.

Debt yield is the blunt instrument: NOI divided by the loan amount, no rate, no amortization, no appraisal. A 10 percent debt yield requirement on 650,000 dollars of NOI caps the loan at 6.5 million regardless of what the appraiser says or where rates sit. Lenders lean on it precisely because it cannot be flattered. There is no assumption inside it to negotiate. It is the constraint that survived 2008 and the one that quietly took over term sheets afterward.

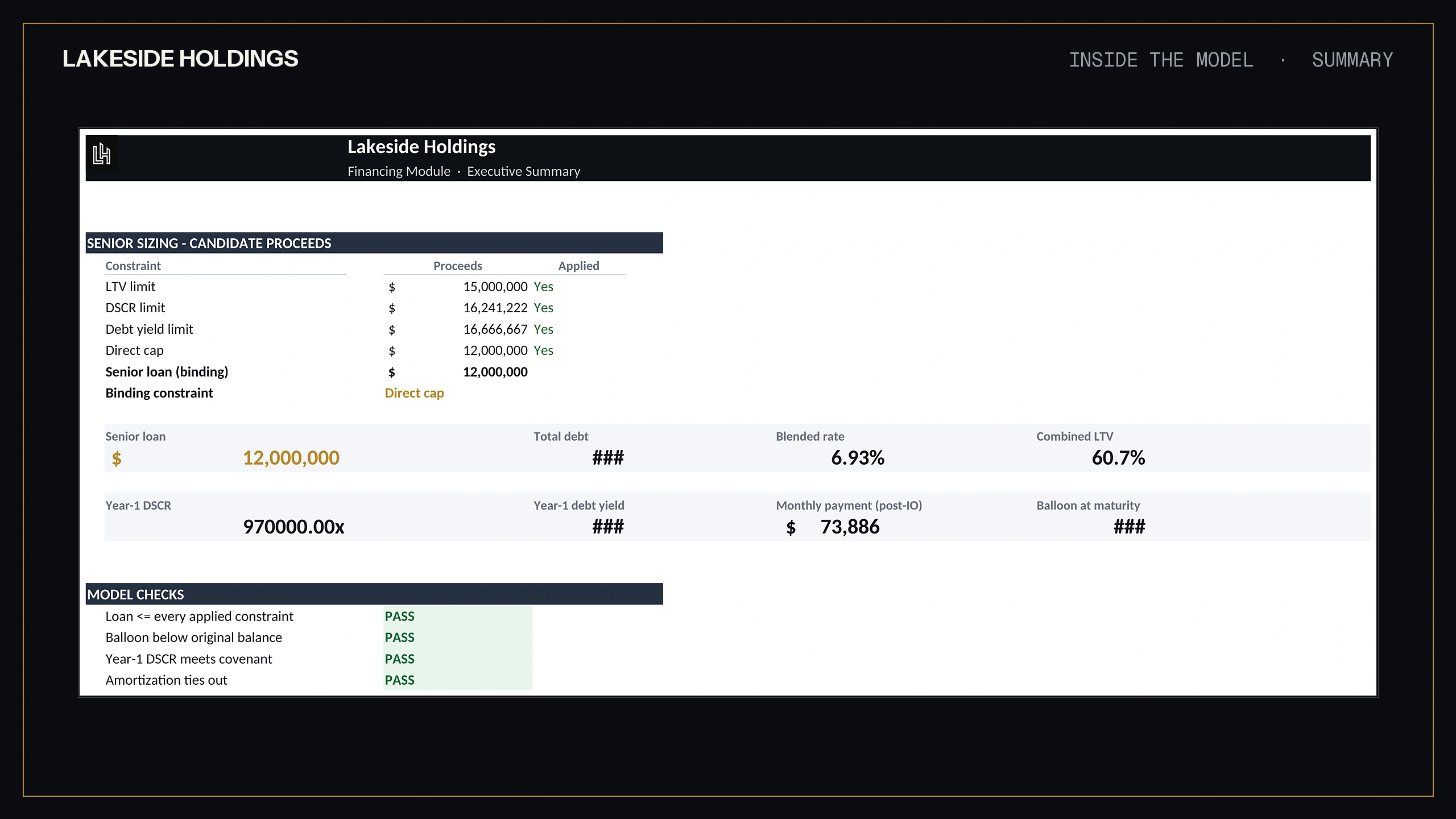

Value 10 million. NOI 650,000, so a 6.5 cap. Rate 6.75 percent, 30 year amortization, which works out to an annual mortgage constant near 7.78 percent. The lender quotes 65 percent LTV, 1.25 coverage and a 10 percent debt yield floor.

Constraint one, LTV: 65 percent of 10 million is 6.50 million.

Constraint two, coverage: maximum debt service is 650,000 divided by 1.25, or 520,000 a year. Divide by the 7.78 percent constant and coverage would allow about 6.68 million.

Constraint three, debt yield: 650,000 divided by 10 percent is 6.50 million.

The binder: LTV and debt yield tie at 6.50 million and coverage would have allowed more. At that loan the deal carries roughly a 1.29 coverage ratio, comfortably above the covenant, which is exactly why anchoring on the coverage quote would have overestimated proceeds by nearly 200,000 dollars.

Now move one number that has nothing to do with the building. Take the rate to 7.5 percent. The constant climbs to about 8.39 percent, the same 520,000 of allowable debt service now supports only about 6.20 million and coverage takes over as the binding constraint. The loan just shrank by roughly 300,000 dollars, the effective leverage fell to 62 percent and the appraisal never changed. Your proceeds are a rate bet whether you like it or not. The only question is whether you priced the bet before the lender did.

Size to the binding constraint, then stress the rate 75 basis points and see whether the binding constraint changes. That second step is the one most models skip, and it is the one that matters.

If the binder is stable under stress, your proceeds are anchored to something durable, the appraisal or the debt yield floor, and a rate move costs you spread but not loan dollars. If the binder flips from LTV to coverage under stress, as it does in the example above, then your refinance story needs work before your acquisition story does. The loan you are modeling in year five assumes a rate environment you do not control, and the gap between the two binders is the size of the equity check you might be writing at the refi table. That number belongs on the same screen as the base case, not in a scenario tab nobody opens. The same discipline applies to the exit assumption, which is its own essay, and the exit cap essay walks the arithmetic.

There is a second habit worth stealing from lenders. When a deal is marketed at a cap rate near or below the mortgage constant, coverage math gets tight fast, because the property's yield barely clears the cost of carrying the debt. The spread between cap rate and constant is a one-second screen for whether leverage is helping or hurting. In the example, a 6.5 cap against a 7.78 constant means every dollar borrowed yields less than it costs to service. Negative leverage is not automatically a dealbreaker, but it should never be a surprise.

When we audit a model, the debt sizing tab is a reliable source of quiet optimism. The patterns repeat. A loan amount hard-coded from the term sheet's LTV quote with no coverage or debt yield test behind it, so the model cannot notice when a rate assumption breaks the sizing. A single constraint tested at close but not at refinance, which is where the flip actually bites. Debt service computed on interest-only terms for the full hold when the term sheet grants two years of IO, which flatters coverage in exactly the years the covenant tests it. And the honest classic: a sensitivity table that stresses rents and vacancy in fine grain while the rate, the input that resizes the whole capital stack, sits frozen.

None of these are fraud. They are defaults nobody challenged. The fix is structural: build the sizing so all three constraints compute live, the binder is flagged and a 75 basis point stress sits next to the base case permanently. That is how the Financing Module in our library is built, it runs all three constraints with toggles, flags the binder and tests covenants for ten years. When the file is somebody else's, checking this is part of how we audit a model, and every audit is verified against an independent replica before release.

Before you circulate proceeds to investors, state the sizing as a sentence: "Our loan is set by the appraisal, and if rates move 75 basis points it will be set by cash flow instead, at a number 300,000 dollars smaller." If you can finish that sentence with your deal's own numbers, your capital stack is underwritten. If you cannot, the term sheet knows something your model does not. The free screener will run the three constraints on any deal in five minutes, and the models in the library carry the full ten-year covenant test.

Three constraints walk into a term sheet. Only one of them sets your proceeds. Find it before it finds you.

The model decides the deal.

We use an essential cookie to remember your preferences and privacy-first analytics that collect no personal data. By continuing you accept our Cookies Policy.We use one essential cookie and privacy-first analytics. Read the Cookies Policy.