Insights · Waterfalls · July 2026 · 7 min

The Waterfall Must Allocate Exactly 100 Percent.

A waterfall that allocates 99 percent of a dollar is broken and one that allocates 101 percent is worse. What to trace before you sign the agreement.

A waterfall that allocates 99 percent of a dollar is broken and one that allocates 101 percent is worse. What to trace before you sign the agreement.

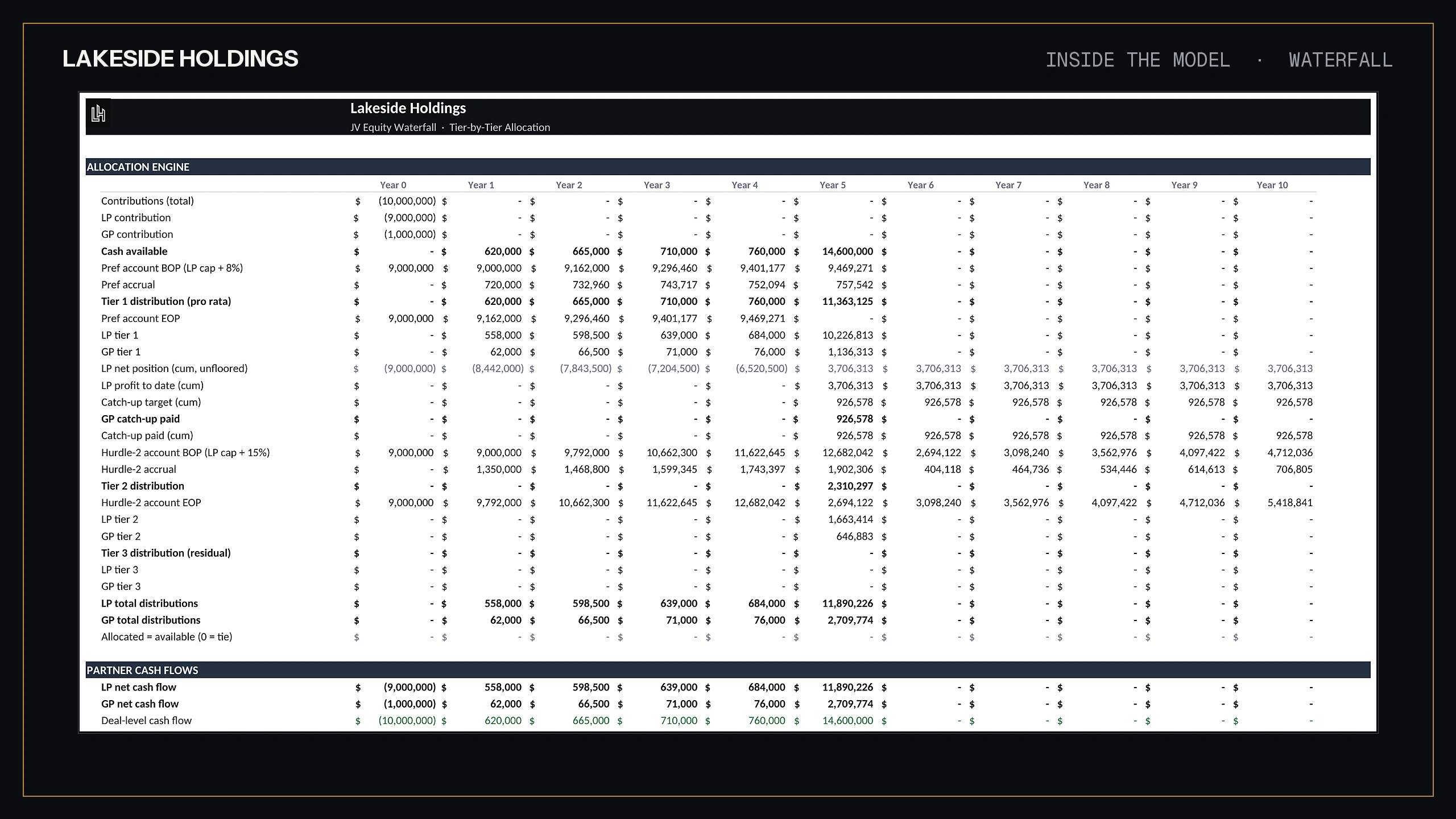

Two partners can share one deal, one set of cash flows and one exit, and walk away with completely different outcomes. The waterfall decides, and most people signing operating agreements have never traced a dollar through theirs. That is the definition problem. The audit problem is worse. When we rebuild a sponsor's model in a second engine, the waterfall tab is where disagreements cluster, and the tell is almost always the same: the tiers do not sum to the money. A waterfall has one non-negotiable property. Every dollar distributed must land in somebody's account, no dollar may land in two, and the tier totals must add back to total distributions exactly. Not approximately. Exactly. A waterfall that allocates 99.7 percent of the cash has not made a rounding error. It has made a promise the operating agreement cannot keep.

Cash comes back from a deal and fills buckets in a fixed order. The names vary by agreement, the structure rarely does.

First, the preferred return. A minimum owed to capital before anyone earns a promote, stated as an annual percentage on unreturned capital. The two questions that matter are whether unpaid pref compounds and from what date it accrues. Those two answers move more money than the headline rate.

Second, return of capital. Everyone gets their basis back. Whether this comes before or after accrued pref, and whether operating cash or only capital events can return capital, are drafting choices with real dollar consequences at the end of a hold.

Third, the catch-up. Once capital has its pref and its basis, many agreements give the GP all or most of the next distributions until the GP's share of total profits reaches the agreed number, commonly 20 percent. The catch-up exists to make the pref a floor rather than a permanent tax on the GP's economics. Its presence or absence is the single most consequential clause most LPs never ask about, and the worked example below puts a number on it.

Fourth, the promote tiers. Above the catch-up, remaining distributions split at the agreed ratio, often 80/20, sometimes shifting further in the GP's favor as higher return hurdles clear. On a home run deal the top tier governs most of the dollars, which is why LPs who only negotiated the pref got the least important number right.

Those are the buckets. The order they fill in, period by period, is its own subject with its own six-figure worked example, and it gets its own essay.

One deal, two waterfalls. An LP invests 10 million. The deal distributes 650,000 a year for four years of operations, then 15 million at exit in year five, 17.6 million in total, 7.6 million of profit. The pref is 8 percent accruing on unreturned capital, unpaid pref carried forward without compounding to keep the arithmetic legible. Capital returns at exit. Above the pref and return of capital, profits split 80/20. The only difference between the two structures is one clause.

Structure A has a 100 percent catch-up to 20 percent of profits. Each operating year the pref accrues 800,000 and cash covers 650,000, so 150,000 carries forward each year and 600,000 of accrued pref enters year five alongside the final 800,000 accrual. At exit the 15 million pays the 1.4 million of accrued pref, returns the 10 million of capital, then the catch-up pays the GP 100 percent of the next 1.0 million, which is the point where the GP's share of all profit distributions reaches 20 percent. The remaining 2.6 million splits 80/20. The GP finishes with 1.52 million, exactly 20 percent of the 7.6 million profit. The LP finishes with 16.08 million, a 1.608x multiple and an 11.04 percent IRR.

Structure B is identical with the catch-up deleted. Same pref, same return of capital, then straight to 80/20. The GP finishes with 720,000, which is 9.5 percent of profit, not 20. The LP finishes with 16.88 million, a 1.688x multiple and a 12.19 percent IRR.

Same deal, same 13.19 percent deal-level IRR, same 17.6 million distributed, and one clause moved 800,000 from one partner's account to the other's. Neither structure is wrong. A GP signing B has agreed that the pref is a tax on its promote forever. An LP signing A has agreed that the pref is only a floor. Both are legitimate positions. The only illegitimate position is not knowing which one you signed. And note the audit property held in both runs: 16,080,000 plus 1,520,000 and 16,880,000 plus 720,000 each sum to 17,600,000 to the dollar. That is what a waterfall that works looks like.

Does the pref compound, and from when. Simple interest on unpaid pref and compound interest on unpaid pref diverge every year the deal runs long, and long is when the pref matters most.

Is the catch-up 100 percent, and to what target share. The example above is the price tag on this clause. A 50 percent catch-up sits between the two structures, and "no catch-up" should be priced, not assumed.

Are hurdles measured on IRR alone, or does an equity multiple floor apply. IRR rewards speed. A fast flip can clear an IRR hurdle while returning very little absolute profit, and a multiple floor is how LPs keep a quick exit from paying like a great hold. The answers to all three move real money at every exit, and none of them are visible in a pitch deck summary.

The waterfall failures we find in audits are rarely exotic. The tiers are built as separate formulas that were each edited separately, so a dollar of exit proceeds gets picked up by two tiers, or by none, and the model distributes 100.4 percent of the cash without anyone noticing because no cell checks the sum. The catch-up is modeled as a fixed 20 percent of profits rather than a balance that fills, which quietly pays the GP its promote on deals that never cleared the pref. Accrued pref restarts at each capital event instead of carrying, which flatters the GP on any deal with a refinance in the middle. And the honest classic: the waterfall was built for the base case and the sensitivity table reruns NOI but not the tier logic, so the downside scenarios print splits that the operating agreement would never produce.

None of these are fraud. They are defaults nobody challenged, sitting in the tab that decides who gets rich. The structural fix is a waterfall built on account balances that fill and spill in order, with one audit row that sums every account against total distributions and flags any penny of daylight. That is how the JV Equity Waterfall engine in our library is built, pref, catch-up and tiers with every account balance visible year by year, and it is one of the checks we run when we audit a model. Every model we publish is verified against an independent replica before release. The same discipline applies to the debt side of the stack, and the debt sizing essay walks that arithmetic.

Before you sign, state your waterfall as a sentence: "On a deal that returns 1.7x, my account receives this many dollars, and if the deal returns only the pref, it receives that many." If you can finish that sentence with your agreement's own numbers, you have read your waterfall. If you cannot, your partner has. Paste your cash flows into the engine and read your own agreement before your partner does. The free screener and the models are on the site.

The waterfall decides who gets rich. The model decides the deal.

We use an essential cookie to remember your preferences and privacy-first analytics that collect no personal data. By continuing you accept our Cookies Policy.We use one essential cookie and privacy-first analytics. Read the Cookies Policy.