Insights · Underwriting · July 2026 · 6 min

The NOI Bridge, Recomputed Line by Line.

How to calculate NOI in real estate line by line on a 100 unit building, from gross potential rent to 676,242, and the 25,000 error worth 385K of price.

How to calculate NOI in real estate line by line on a 100 unit building, from gross potential rent to 676,242, and the 25,000 error worth 385K of price.

Net operating income is the number everything else rides on. The cap rate multiplies it, the loan sizes to it, the waterfall distributes what is left of it, and a 25,000 dollar error in it becomes roughly 385,000 dollars of price at a 6.5 percent cap rate. That exchange rate is the whole reason NOI deserves more care than any other line in the model. This essay defines NOI, builds one from the ground up on a real example with every assumption stated, and shows where the errors that survive to closing like to hide.

NOI is all income a property actually produces, minus the expenses required to operate it, before debt service and before capital items. The formula is one line: effective gross income less operating expenses. The discipline is two lists, what goes in and what stays out, and most NOI arguments are really arguments about the second list.

In: rental collections, parking, laundry, storage, utility reimbursements, fees. Out: debt service, because NOI describes the property and not your financing. Out: capital expenditures and reserves, because a roof is not an operating cost, it is the property consuming capital. Out: depreciation and income taxes, which belong to the owner's accountant, not the building. Property taxes stay in. That asymmetry between property taxes in and income taxes out is the first thing to check in an unfamiliar statement.

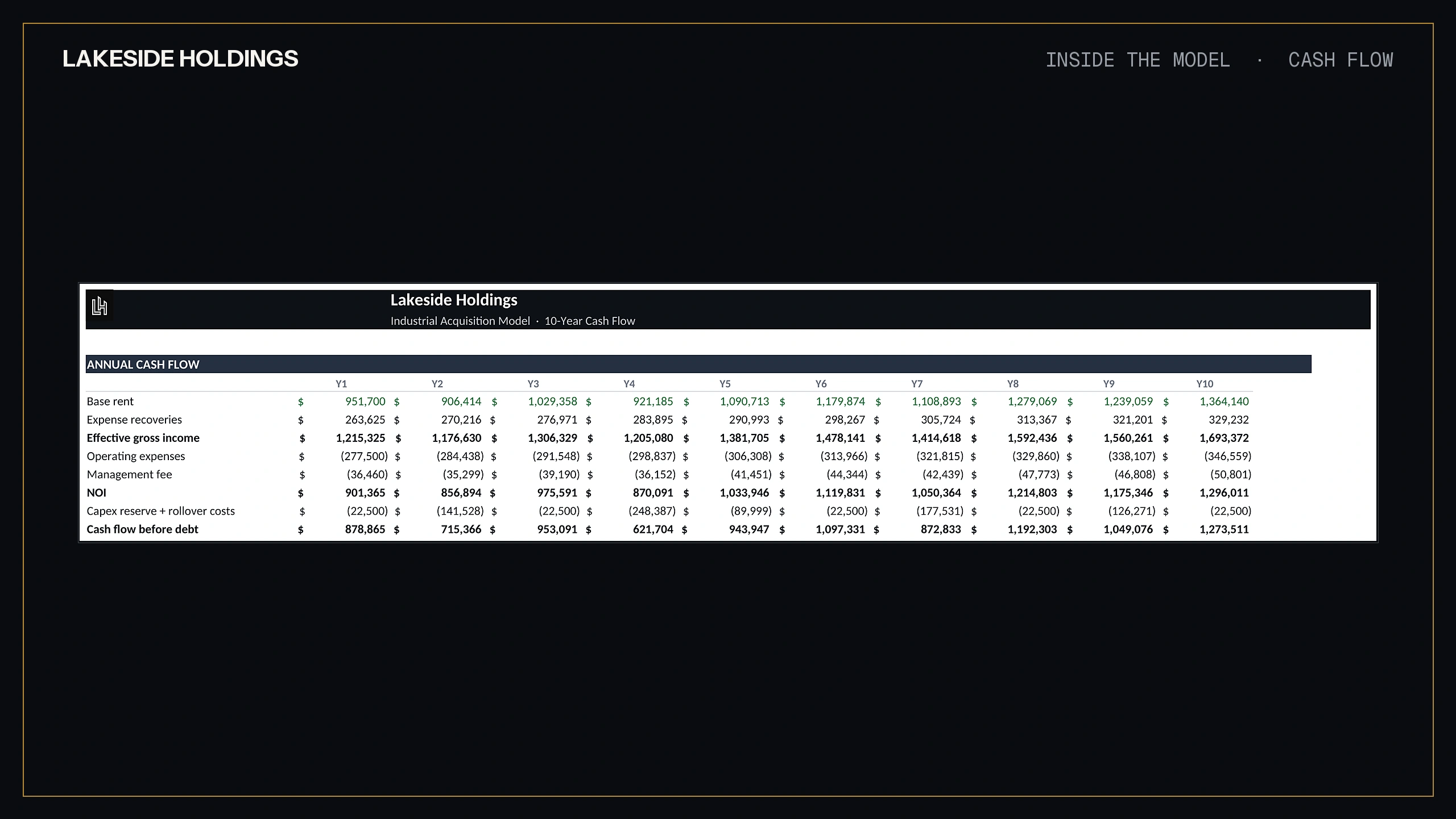

The income side of the bridge fails before the expense side does, because the top line most packages hand you is scheduled rent, not cash. Gross potential rent, less vacancy, less loss to lease, less concessions, less bad debt, less non-revenue units. We walked that exact schedule in the economic occupancy essay: a 100 unit building with 1,440,000 of gross potential rent that is 95 percent full and collects 1,242,600, which is 86.3 percent paid. The building from that essay is the building in this one, carried forward on purpose. NOI built on scheduled rent inherits every one of those gaps at full price, which is why the first step is always to analyze the rent roll and the T-12 before a single expense gets debated.

Add other income honestly. This building runs 36,000 a year of parking, laundry and fees, about 30 dollars a unit a month. Effective gross income is 1,278,600. Other income deserves one skeptical look of its own: fee income that appears for the first time in the pro forma year is a plan, not a property.

Seven lines cover an ordinary multifamily statement. Here they are for this building, stated in full so the total can be checked.

Property taxes, 168,000, and this is the post-sale bill, computed from the jurisdiction's reassessment practice and the millage, not the seller's current bill. Hold that thought for one section. Insurance, 60,000. Repairs and maintenance, 78,000. Payroll, 110,000 for on-site staff. Utilities, 96,000 for common areas and the units the owner carries. Admin and marketing, 52,000. Management at 3 percent of effective gross income, 38,358, and it stays in the bridge even if you plan to self-manage, because the next buyer's lender will put it back.

Total operating expenses: 602,358. That is a 47.1 percent expense ratio and 6,024 per unit, both worth comparing to the comp set before you trust them. NOI: 1,278,600 less 602,358 is 676,242. At a 6.5 cap the building prices at about 10.4 million.

Now the reason the bridge gets recomputed instead of reviewed. The seller's pro forma for this same building shows NOI of 701,242. Every income line matches. Six of the seven expense lines match. The seventh is property taxes at 143,000, the seller's current bill on his old assessment. In many jurisdictions the assessor marks the property to something near the sale price, so the buyer's real bill is the 168,000 we computed. The difference is exactly 25,000 of NOI, which at the 6.5 cap is roughly 385,000 dollars of price. One line, defensible in isolation, quietly asking the buyer to pay 385K for a tax bill that dies at closing.

That is what an NOI error usually looks like. Not fraud, not a broken formula, just one assumption that favors the seller sitting in a column of nineteen that do not. The only way to find it is to rebuild the bridge in a fresh cell block that trusts nothing the model already totaled, then reconcile line by line. If your recomputed NOI and the model's NOI differ by even a dollar, stop and find out why before touching anything downstream. Small unexplained differences are how large hidden ones announce themselves.

Four more spots earn a permanent look. Reserves smuggled above the line in one statement and below it in another, which moves NOI by 250 to 300 a unit and makes two buildings incomparable until you restate them the same way. Management fees deleted because the buyer self-manages, which flatters NOI now and surprises the appraisal later. Utility reimbursements booked as income while the matching expense quietly grew. And the pro forma year itself, where every line is allowed to improve at once and the expense ratio drifts three points below anything the T-12 ever produced.

One habit closes most of the remaining gap: never let the model carry a single number called NOI. Carry two, labeled. In-place NOI is the bridge built from the T-12 and the actual rent roll, the building as it operates today. Pro forma NOI is the same bridge after your plan works, the rents captured, the expenses trimmed, the fee income real. The first number is evidence. The second is a forecast that belongs to you, not the seller. Deals get overpaid for when a pro forma number is priced at an in-place cap rate, because the buyer is then paying today for work nobody has done, at a multiple reserved for certainty. Keep the two columns side by side and make every difference between them a stated assumption with a date on it. Where the plan shows up in the rent line, the loss to lease essay walks how slowly captured rent actually arrives.

When we audit a model, the NOI bridge is rebuilt from source documents in a second engine and reconciled to the dollar, because every downstream tab is decoration until the bridge ties. Every model we publish carries the bridge as explicit rows a reader can check, verified against an independent replica before release.

Before an NOI goes in your model, state it as a sentence: "This building collects this much cash, spends this much to operate, and the tax line is the buyer's bill, not the seller's." If any clause comes from the deal summary instead of the T-12 and the assessor, that clause is your homework. The free screener and the models are on the site.

The bridge ties or it does not. The model decides the deal.

We use an essential cookie to remember your preferences and privacy-first analytics that collect no personal data. By continuing you accept our Cookies Policy.We use one essential cookie and privacy-first analytics. Read the Cookies Policy.