Full Building, Empty Bank Account: Economic Occupancy.

A building can be 95 percent full and 86 percent paid. Both numbers get called occupancy in the deal package, and only one of them pays the mortgage.

A building can be 95 percent full and 86 percent paid. Both numbers are called occupancy, both will appear in a deal package, and only one of them pays the mortgage. The difference between them is the difference between counting bodies and counting dollars, and on an ordinary 100 unit deal it can hide more than two million dollars of value claim. This essay defines both terms, walks one building from the full number to the paid number one line at a time, and shows where each missing dollar went.

The two definitions

Physical occupancy is the percentage of units with a tenant in them. Ninety five occupied units out of one hundred is 95 percent physical occupancy. It is a headcount. It is also the number the leasing office reports, the number on the first page of the offering memorandum and the number everyone quotes at the property tour, because it is the flattering one.

Economic occupancy is the percentage of gross potential rent actually being collected. Gross potential rent is what the building would produce if every unit were occupied at market rent with every tenant paying in full. Economic occupancy divides real collections by that ceiling. It is a cash number, and cash is what services debt and returns capital, which is why the second definition is the one the model should care about.

The two numbers diverge because a unit can be occupied and still not be paying full freight. A tenant behind on rent occupies a unit. A tenant on a concession occupies a unit. A tenant paying last year's rent occupies a unit. A model unit with a leasing agent's furniture in it occupies a unit. Physical occupancy counts all four at full value. Collections do not.

The worked example, assumptions stated

Take 100 units at a market rent of 1,200 a month. Gross potential rent is 1,440,000 a year. Physical occupancy is 95 percent, five units vacant, and the deal summary will print 95 percent in bold. Now walk from the ceiling to the bank account.

Vacancy takes the first cut. Five empty units at market is 72,000 a year. This is the only line physical occupancy admits to.

Loss to lease takes the second. The 95 occupied units pay an in place average of 1,150 against the 1,200 market, a 50 dollar gap that compounds to 57,000 a year. The units are full. The rent is last year's. We wrote a full essay on loss to lease and why that gap converts to cash far more slowly than the deal summary implies, so here it is enough to say the 57,000 is scheduled, not collected.

Concessions take the third. Twenty new leases signed with one month free is 24,000 a year quietly amortizing through the rent roll. On the report date those twenty tenants show contract rent in the rent column. The free month lives somewhere else, usually in a footnote, sometimes nowhere.

Delinquency takes the fourth. Call it 30,000 a year of billed rent that is not arriving, a touch over two percent of scheduled collections, which is unremarkable for a workforce housing deal and optimistic for a distressed one. These tenants are occupants. Physical occupancy counts every one of them.

The model unit takes the fifth. One unit of the 95 is occupied by the leasing office itself, 14,400 a year of rent nobody pays. It has furniture, it shows beautifully and it collects nothing.

Add it up. From a 1,440,000 ceiling the building collects 1,242,600. Economic occupancy is 86.3 percent. The same building, the same rent roll, the same afternoon: 95 percent full, 86.3 percent paid.

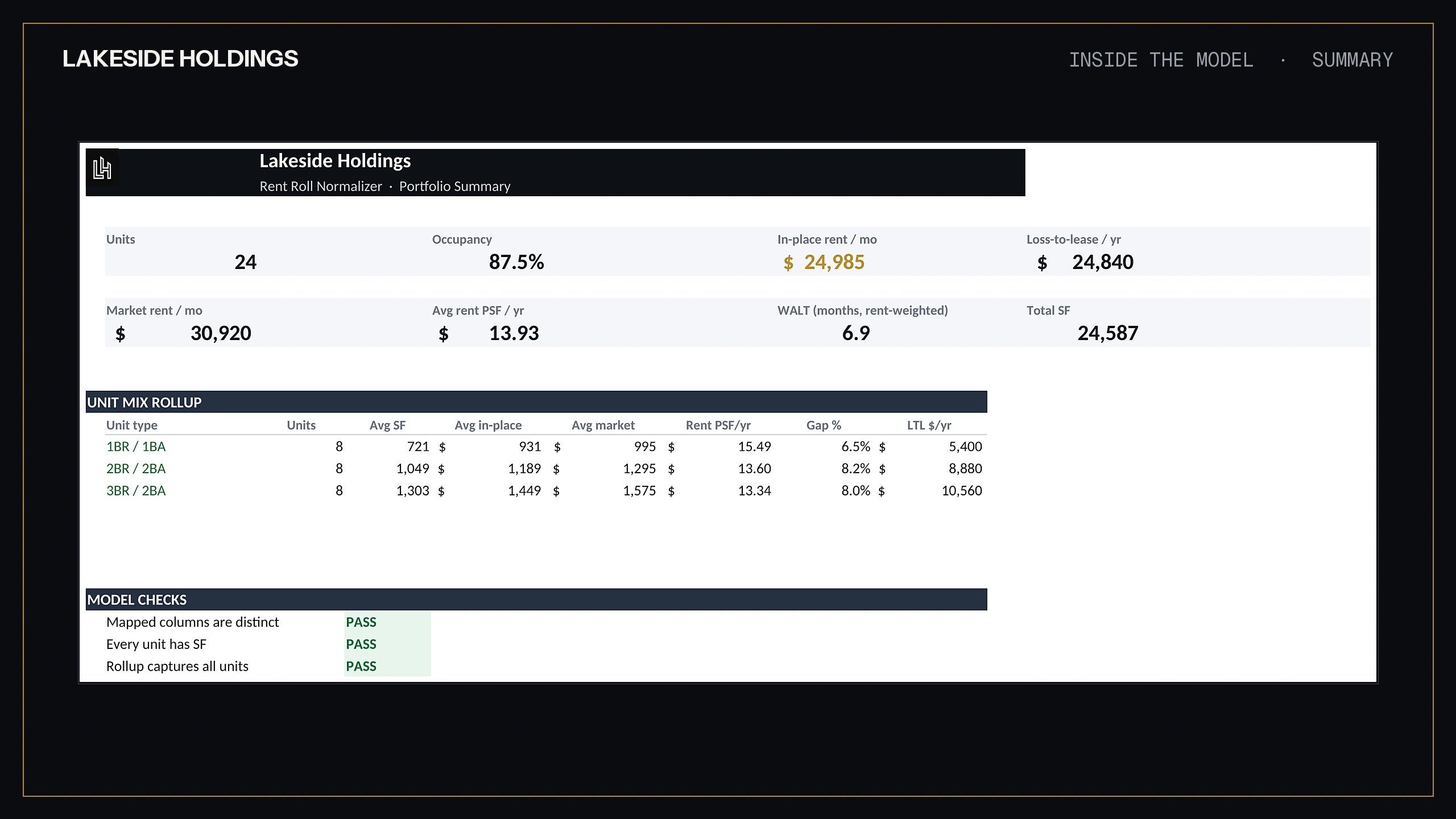

Exhibit · Physical occupancy sitting beside in-place rent, market rent and loss to lease · Rent Roll Normalizer

What the gap costs

The distance between the two readings is not an accounting curiosity. Price the building off scheduled rent at 95 percent physical and you are capitalizing 1,368,000 of revenue. Collections are 1,242,600. The gap is 125,400 a year, and at a 6.0 cap that gap prices at 2.09 million dollars on a building that might trade for twenty. Most of a lost collections dollar falls straight to NOI, because the property's expenses do not drop when a tenant stops paying, so before any small variable expense offset the value error is roughly the full capitalized gap. On this building each point of economic occupancy is worth 14,400 a year, which is 240,000 of value. Points of economic occupancy are expensive. Points of physical occupancy are free, which is exactly why the marketing package prefers them.

How the two numbers get confused on purpose

No seller writes "economic occupancy 86.3 percent" on the first page. The confusion is structural. The rent roll reports contract rent and a unit status column, which produces physical occupancy natively. Producing economic occupancy requires three more documents: the delinquency report, the concession schedule and the trailing twelve months of actual collections. Every one of those documents exists, and none of them is in the first email. The practical rule is simple: any occupancy figure quoted without a T-12 next to it should be assumed physical until proven economic.

The T-12 is the arbiter because collections appear there as cash, after concessions, after bad debt, after the model unit. Divide trailing twelve collections by gross potential rent and you have economic occupancy with no one's opinion in it. If that number and the quoted occupancy are more than a few points apart, the gap has a story, and the story is usually one of the five lines above.

The three checks that take ten minutes

First, compute economic occupancy from the T-12 and gross potential rent before the tour, not after. Second, ask for the delinquency report with the rent roll, always, and tie its total to the bad debt line in the T-12. Third, count the non-revenue units by name: model, office, maintenance, manager's unit. They are in the physical count and out of the cash, and every one of them is a permanent point of gap.

All three checks start from a rent roll forced into one honest format, which is why the first step is always to analyze the rent roll before any occupancy claim gets repeated. Our Rent Roll Normalizer reconciles unit count and scheduled rent to source and reads out the gap between scheduled and collectible line by line. When we audit a model, the occupancy assumption is rebuilt from the T-12 rather than accepted from the summary page, and every model we publish is verified against an independent replica before release.

The one-sentence test

Before an occupancy number goes in your model, state which one it is: "This building is X percent full and Y percent paid, and the model uses Y." If the package only lets you finish the first half of the sentence, the second half is your homework, not the seller's disclosure. The free screener and the models are on the site.

The building was full. The model decides the deal.

Put it to work

The models behind these essays are in the library.

We use an essential cookie to remember your preferences and privacy-first analytics that collect no personal data. By continuing you accept our Cookies Policy.We use one essential cookie and privacy-first analytics. Read the Cookies Policy.