Insights · Screening · July 2026 · 6 min

Five Minutes Before You Fall in Love With a Deal.

Every deal deserves five minutes and few deserve a week. One deal walked through our free screener, assumptions stated, with the verdict included.

Every deal deserves five minutes and few deserve a week. One deal walked through our free screener, assumptions stated, with the verdict included.

Every deal deserves five minutes. Few deserve a week. The difference between the two is a screen, and the best use of a screen is saying no faster, before the tour, before the data room, before the part of your brain that already pictured the closing dinner starts negotiating with your underwriting. This essay walks one deal through our free screener, assumptions stated, and shows what a disciplined first cut looks like and why the verdict is usually decided by one assumption you have not questioned yet.

A screener is not underwriting. It is triage. Full underwriting rebuilds the rent roll, recomputes the NOI bridge and traces the waterfall, and it earns that effort only after a deal survives the first cut. The first cut needs exactly four inputs, price, income, expenses and debt terms, plus one thing most screens skip: your hurdles, stated in advance. A minimum IRR and a minimum DSCR, typed in before you see the answer, so the verdict belongs to the numbers and not to your mood on the day the package arrived.

That is how our free screener is built. Enter the deal, set your own hurdles, and it returns a clean PENCILS or PASS verdict with the numbers that drive it: cap rate, DSCR, cash-on-cash, levered IRR and equity multiple over a hold you choose. Growth, exit cap and sale costs are all adjustable, which matters, because the verdict is going to hinge on them.

Here is a deal that looks the way deals look at the tour. Asking 5.0 million with 325,000 of year one NOI, a 6.5 cap in a market where that is a fair print. Debt at 65 percent of price, 6.75 percent, 30 year amortization. The mortgage constant works out to 7.78 percent and debt service to 252,953 a year. Coverage is 1.28, comfortably over a 1.25 requirement. Equity with 2 percent closing costs is 1.85 million, and year one cash flow of about 72,000 is a 3.9 percent cash-on-cash.

Set the hurdles before running it: 15 percent levered IRR minimum, 1.25 DSCR minimum. Hold five years, grow NOI at 2.5 percent, exit at a 7.0 cap, half a point wider than entry because five years is a long time to promise today's pricing, pay 2 percent to sell.

The screen comes back in one page. DSCR passes at 1.28. The exit clears the loan balance of roughly 3.05 million for net proceeds just under 2.1 million. Levered IRR: 7.05 percent. Equity multiple: 1.37. Verdict against your stated hurdles: PASS, as in pass on it. The deal that passed every number a broker quotes at a property tour just failed the only two numbers you promised yourself in advance.

A screen that says no is not the end of the analysis. It is the start of the only conversation worth having, which is: what would have to be true for this to pencil. The screener makes that question precise, because the inputs are sitting in front of you and each one can be pushed.

Push the price. Holding everything else, the IRR reaches 15 percent at about 4.39 million, a 7.4 cap, roughly 12 percent and 614,000 dollars below ask. That is not an insult, it is a bid with arithmetic behind it. Push the exit cap instead. Even selling at a 6.0, tighter than you bought, the deal only reaches 13.8 percent at full ask. That is worth knowing before the tour: this deal cannot reach your hurdle at this price under any exit assumption you would defend in writing, so the negotiation is about price or it is about nothing. The exit cap does most of the work in any five year IRR, and a screen that lets you move it openly is the difference between an assumption and a hope.

Five minutes. One page. You now know the deal fails your hurdles at ask, you know the price at which it stops failing, and you know the story a seller would need you to believe. Most people spend a week getting less.

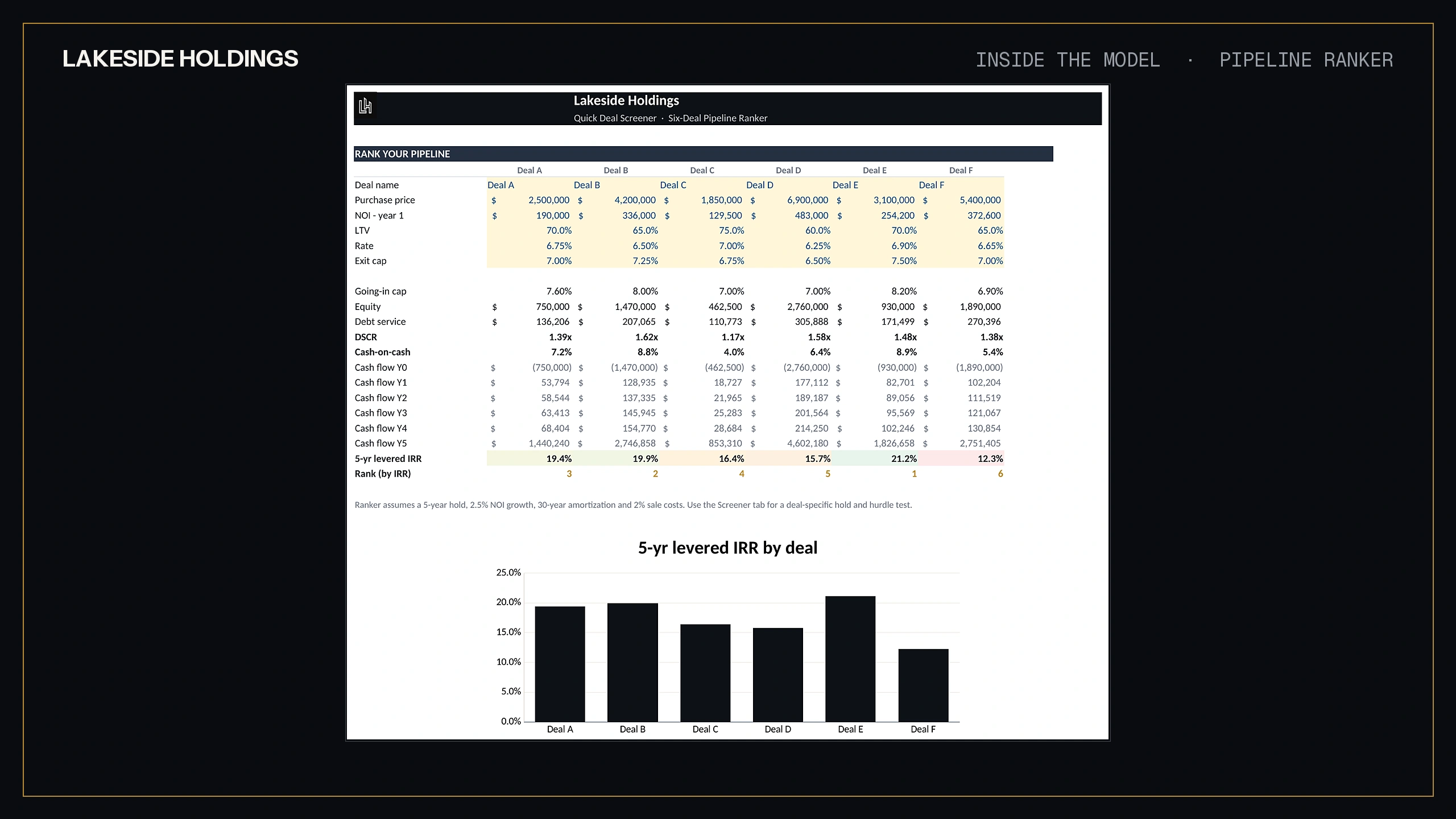

The second discipline a screener enforces is comparison. A deal examined alone is negotiating with your enthusiasm. A deal ranked against five others is negotiating with your alternatives. The screener's Pipeline Ranker stacks six deals side by side, ranked by levered IRR, which turns the question from "do I like this deal" into "is this the best use of the same equity this quarter". Deals die faster and better that way. The preloaded sample pipeline shows the format before you commit your own numbers to it.

A screen that says PENCILS earns the deal a week of real work, which means the rent roll, the T-12 and eventually someone to audit a model before capital commits. The screen is the gate, not the decision. But the gate is where discipline is cheapest, because saying no in five minutes costs nothing and saying no after three weeks of underwriting never quite happens.

A screen is only as honest as the four numbers you feed it, and at the five minute stage those numbers came from the deal package. That means the screen inherits every flattering assumption in it. The income line is probably scheduled rent rather than collections, so a building that is full but not paid walks through the gate looking healthier than it is. The expense line is probably the seller's, with his old tax bill still in it. The screener cannot catch that, and pretending otherwise would make it a worse tool, not a better one.

So use the verdicts asymmetrically. A PASS at the package's own numbers is close to final, because a deal that fails on the seller's best case does not improve when you rebuild the NOI from source. A PENCILS is provisional, an invitation to spend the week verifying the inputs the screen took on faith: analyze the rent roll, recompute the NOI bridge with the buyer's tax bill, restate the income at economic rather than physical occupancy. The screen decides which deals earn that work. It never replaces it, and a tool that claims to do both in five minutes is lying about one of them.

That division of labor is the whole design. Five minutes to say no with arithmetic, a week to say yes with evidence, and every model in the library, the screener included, is verified against an independent replica before release.

Before you spend a week on a deal, finish this sentence: "At my hurdles, stated in advance, this deal pencils at this price under these assumptions." If you can finish it, the week is justified. If you cannot, the deal has not earned the week, whatever the brochure says. The free screener is on the site with the rest of the models, and the verdict it prints is yours, because the hurdles were.

Five minutes first. The model decides the deal.

We use an essential cookie to remember your preferences and privacy-first analytics that collect no personal data. By continuing you accept our Cookies Policy.We use one essential cookie and privacy-first analytics. Read the Cookies Policy.